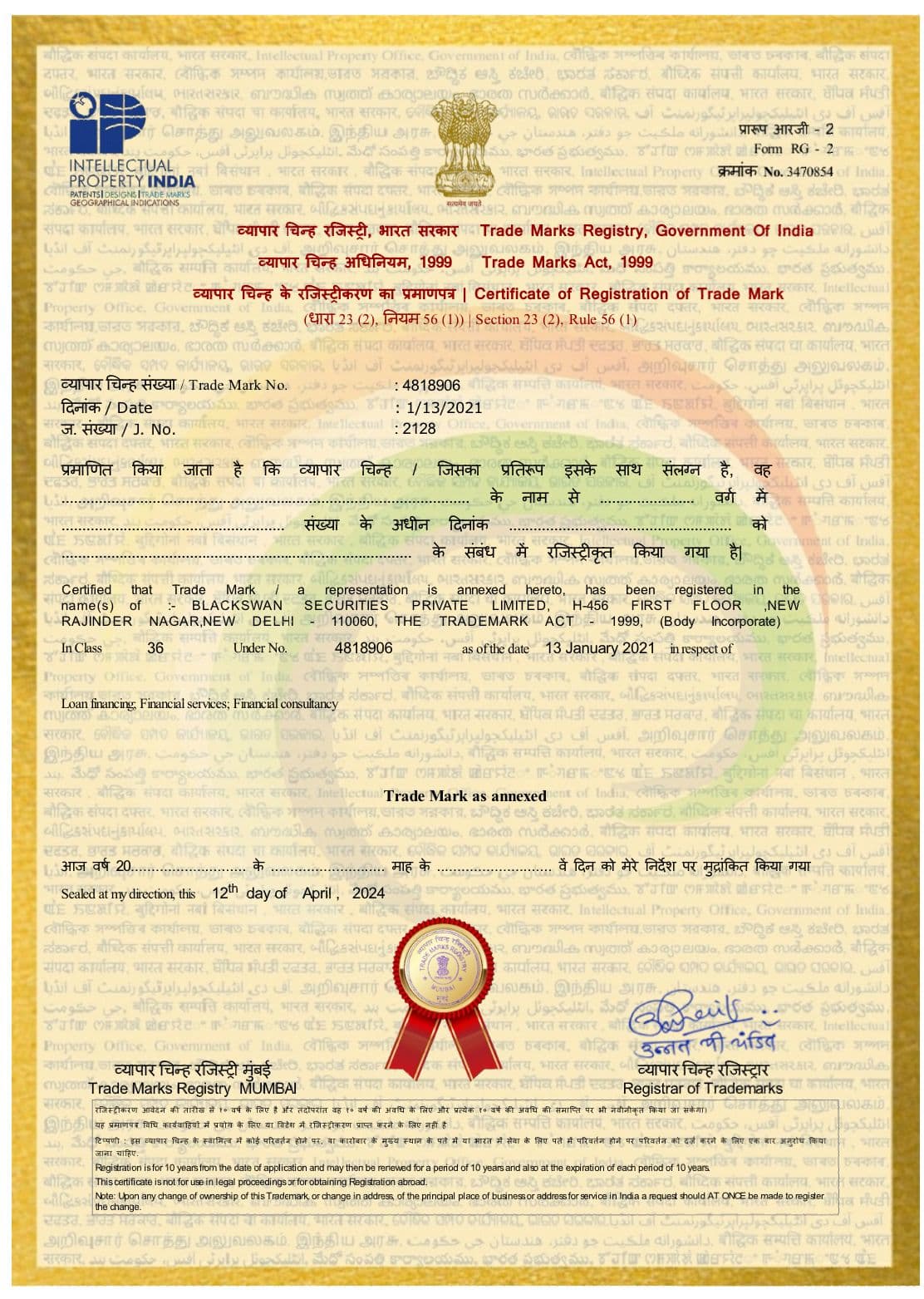

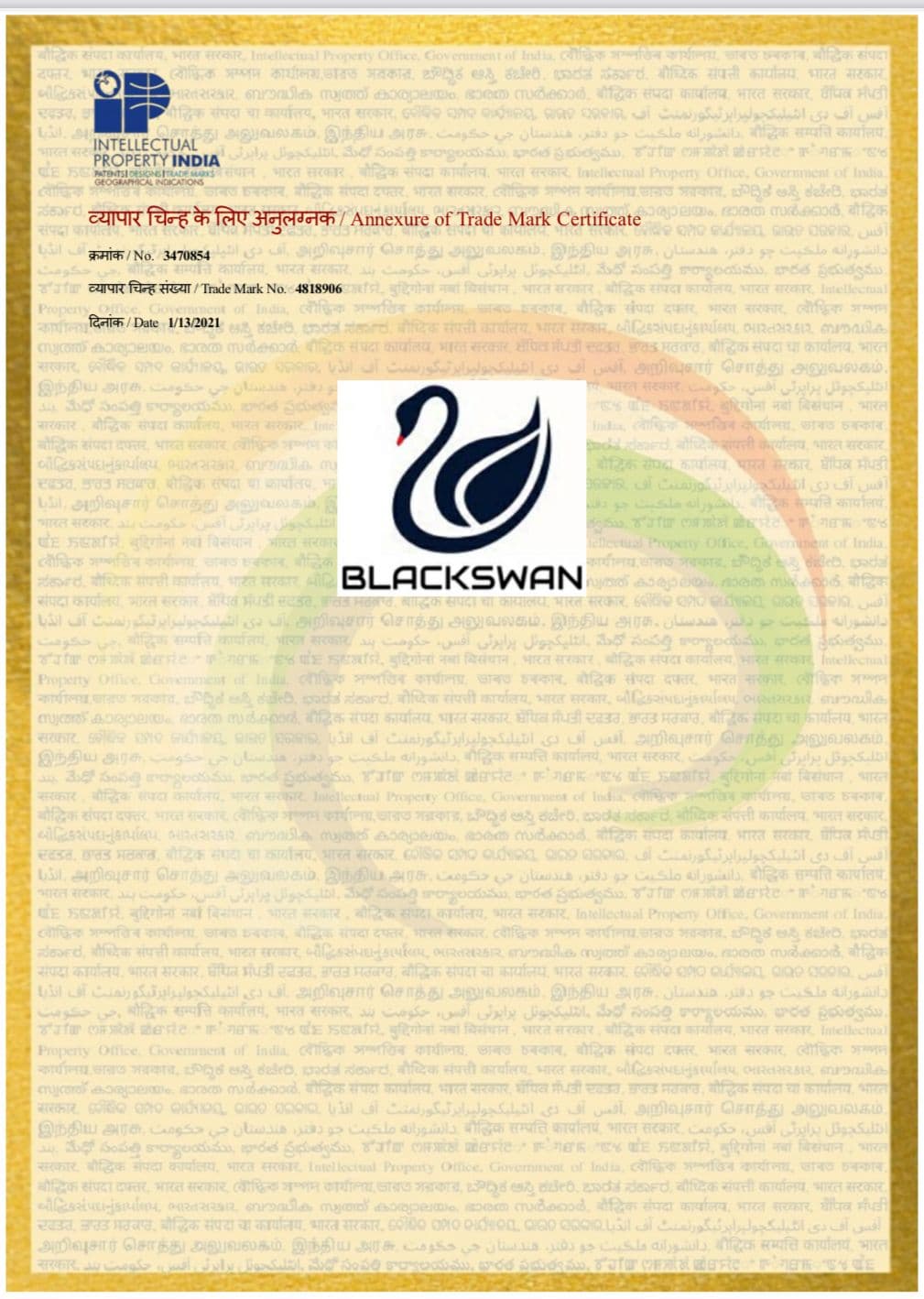

BlackSwan® Securities India

At BlackSwan® Securities India, we empower your financial journey with expert wealth management and personalized financial planning. Our core offerings include a diverse range of portfolio management funds and alternative investment funds, carefully curated to match your risk appetite, goals, and financial profile.

What is a Black Swan Event?

A Black Swan Event refers to a rare and unpredictable occurrence that has a massive impact on financial markets, economies, or global systems. These events are extremely difficult to predict using traditional financial models or historical market data.

Rarity

The event lies outside normal expectations and is extremely rare. Most investors and analysts do not anticipate such events.

Extreme Impact

When the event occurs, it causes major disruption in financial markets, global economies, and investor portfolios.

Retrospective Explanation

After the event happens, people often attempt to explain it as if it was predictable, even though it was not anticipated before.

Why It Matters for Investors

Black Swan events such as the 2008 global financial crisis or the COVID-19 pandemic show how unexpected shocks can rapidly reshape financial markets. Because these events are difficult to predict, investors often focus on diversification and disciplined portfolio strategies to manage uncertainty.

Expertise in AIF & PMSInvestment Solutions

At BlackSwan Securities, we leverage 15+ years of capital markets expertise to curate India’s best AIF and PMS funds on a single platform. Our rigorous due diligence process identifies top funds with proven performance across market cycles.

Our AIF and PMS strategies prioritize capital protection through rigorous risk management frameworks, ensuring your wealth grows safely even in volatile markets.

Monitor all your PMS and AIF investments in one secure dashboard with real-time tracking for effortless portfolio management at BlackSwan Securities.

Get exclusive access to expert commentary and performance reports from top fund managers, all under one trusted platform at BlackSwan Securities.

👉 Built for HNIs seeking disciplined, research-led investment decisions

I founded BlackSwan Securities with a simple mission to provide honest, transparent, and high-performance wealth solutions. In an industry often clouded by conflicts of interest, I believe in putting clients first always. Whether you're an investor seeking tailored PMS strategies or exploring high-potential AIF opportunities, my team and I are committed to aligning your capital with the right opportunities. At BlackSwan, we don’t just manage wealth; we build trust. Because true success isn’t just about returns—it’s about integrity, discipline, and long-term partnerships.

Founder & CEO, BlackSwan Securities

Blackswan Securities

We have done some

great work

100+

PMS

50+

AIF's

2500+

Active Clients

500+

Mutual Funds

Industry Recognition

We began our journey in 2014 with a promise to deliver high-performance investing. These awards stand as a testament to our efforts over the past five years.

Trusted and certified

Compare Your Options

Quick side-by-side clarity for investors evaluating PMS, AIF, and mutual funds.

PMS vs Mutual Funds

- -Minimum ticket: PMS starts at INR 50 lakh; mutual funds start much lower.

- -Ownership: PMS holds stocks in your demat; mutual funds are pooled units.

- -Control: PMS can be customised and concentrated; mutual funds stay diversified.

- -Fees: PMS mixes fixed + performance fees; mutual funds charge an expense ratio.

AIF vs PMS

- -Structure: AIFs are pooled trusts; PMS is a segregated, client-specific account.

- -Flexibility: AIFs access complex strategies; PMS focuses on listed equities.

- -Liquidity: PMS typically T+1/T+2 exit; AIFs may have lock-ins and gates.

- -Suitability: AIFs fit thematic/alternatives; PMS fits bespoke equity portfolios.

FAQs

Who does BlackSwan Securities serve?+-

What makes BlackSwan’s advice different?+-

How do you shortlist PMS/AIF managers?+-

How do I start with BlackSwan?+-

Trusted AIF & PMS Investment Experts

SEBI-registered Alternative Investment Funds and Portfolio Management Services for long-term wealth creation.

SEBI Registered

Only SEBI-Registered PMS & AIF Strategies.

Expert Advisory

Personalized AIF & PMS for HNIs & NRIs.

Highest Compliance

SEBI-Compliant AIF & PMS for Risk-Adjusted Alpha.

Ready to take your portfolio to the next level?

Schedule a ConsultationCall us at +91 85950 41463